The Hong Kong market has recently experienced a significant boost, driven by China’s robust stimulus measures aimed at revitalizing its economy. Amid this positive backdrop, investors are increasingly looking for growth companies with high insider ownership and strong earnings potential. In the current market environment, stocks that demonstrate substantial insider ownership often signal confidence from those who know the company best. This article will explore three such growth companies listed on the SEHK that have achieved an impressive 25% earnings growth.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

|

Name |

Insider Ownership |

Earnings Growth |

|

Laopu Gold (SEHK:6181) |

36.4% |

32.7% |

|

Akeso (SEHK:9926) |

20.5% |

54.5% |

|

Fenbi (SEHK:2469) |

33.1% |

22.4% |

|

Zylox-Tonbridge Medical Technology (SEHK:2190) |

18.8% |

69.8% |

|

Pacific Textiles Holdings (SEHK:1382) |

11.2% |

37.7% |

|

RemeGen (SEHK:9995) |

16.1% |

52.2% |

|

Zhejiang Leapmotor Technology (SEHK:9863) |

15% |

78.9% |

|

DPC Dash (SEHK:1405) |

38.1% |

104.2% |

|

Beijing Airdoc Technology (SEHK:2251) |

29.1% |

93.4% |

|

Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) |

13.9% |

109.2% |

Let’s take a closer look at a couple of our picks from the screened companies.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kuaishou Technology, an investment holding company with a market cap of HK$236.57 billion, provides live streaming, online marketing, and other services in the People’s Republic of China.

Operations: Revenue Segments (in millions of CN¥): Domestic: 117.32 billion, Overseas: 3.57 billion

Insider Ownership: 19.4%

Earnings Growth Forecast: 18.7% p.a.

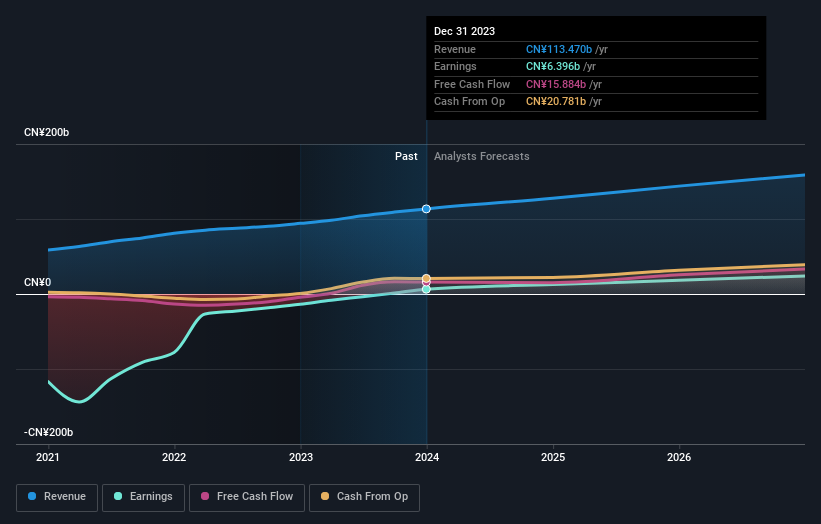

Kuaishou Technology, a growth company with high insider ownership in Hong Kong, has shown robust revenue and earnings growth. Recent results for Q2 2024 reported CNY 30.98 billion in sales and CNY 3.98 billion in net income, marking significant year-over-year increases. The company’s AI advancements, particularly the Kling AI video generation model, have been well-received, enhancing user engagement and commercial potential. Analysts forecast its earnings to grow faster than the market at 18.69% per year.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited, with a market cap of HK$926.83 billion, operates in the automobiles and batteries sectors across China, Hong Kong, Macau, Taiwan, and internationally.

Operations: Revenue segments (in millions of CN¥) for BYD Company Limited are as follows: Automobiles and Related Products and Other Products: ¥507.52 billion, Mobile Handset Components, Assembly Service and Other Products: ¥154.49 billion.

Insider Ownership: 30.1%

Earnings Growth Forecast: 15.2% p.a.

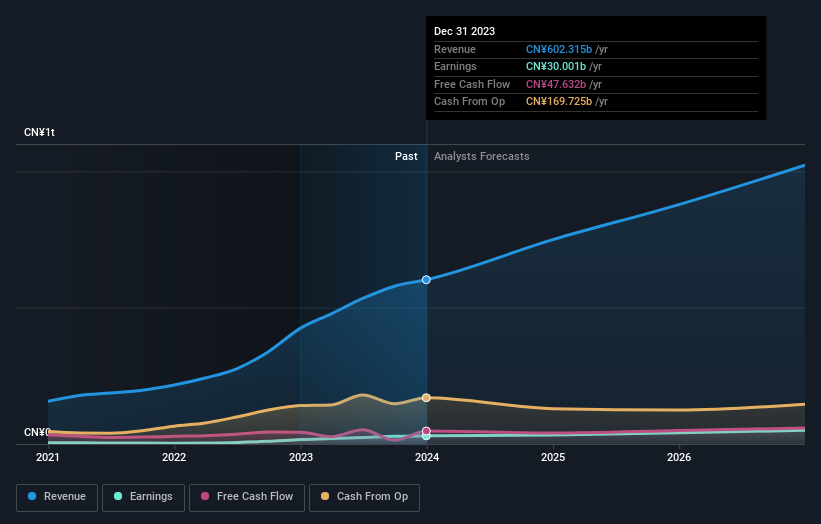

BYD has demonstrated substantial growth with high insider ownership. Recent unaudited results for August 2024 show production and sales volumes of 2.32 million units year-to-date, up from 1.83 million and 1.55 million units respectively a year ago. The company reported half-year sales of CNY 294.77 billion and net income of CNY 13.63 billion, reflecting strong performance metrics in its sector. Analysts forecast BYD’s earnings to grow at an annual rate of 15.23%, outpacing the Hong Kong market average.

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Meituan operates as a technology retail company in the People’s Republic of China with a market cap of approximately HK$1.02 trillion.

Operations: The company’s revenue segments include Core Local Commerce generating CN¥228.13 billion and New Initiatives contributing CN¥77.56 billion.

Insider Ownership: 11.8%

Earnings Growth Forecast: 26% p.a.

Meituan has shown robust growth with high insider ownership. The company reported half-year sales of CNY 155.53 billion and net income of CNY 16.72 billion, both significantly up from the previous year. Analysts forecast annual earnings growth of 26%, outpacing the Hong Kong market average. Recent buybacks totaling HKD 7,173.7 million indicate strong confidence in its future prospects despite slower revenue growth projections compared to other high-growth companies.

Taking Advantage

Contemplating Other Strategies?

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include SEHK:1024 SEHK:1211 and SEHK:3690.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Read More: 3 SEHK Growth Companies With High Insider Ownership And 25% Earnings Growth