The yield curve moved further toward un-inversion, but not the way it was hoped.

By Wolf Richter for WOLF STREET.

The Treasury yield curve un-inverted by another big step on Friday: The three-month yield has vacillated in the same range for the past 11 trading days following the drop after the monster rate cut. But longer yields surged, starting with the one-year yield, with rate cut expectations getting slashed, and with inflation fears returning. This nearly fixed position at the short end and surge in yields further out on the yield curve caused it to un-invert by another step, but not the way folks had hoped.

Folks – especially the real estate industry – had hoped that the yield curve would un-invert amid a series of steep rate cuts that would bring down short-term yields fast, and that long-term yields would follow but more slowly, so that yields would be lower across the curve than they’d been before the rate cut, but with short-term yields a lot lower and long-term yields somewhat lower, and mortgage rates lower too.

But longer-term yields had never fully bought into the rate hikes in the first place, with the 10-year yield remaining well below the Fed’s policy rates; and then they started dropping in November last year in expectations of lots of rate cuts – reinforced by the labor market tail spin in July and August that has now turned out to have been a false alarm – and very low inflation in the future that has now come back into question.

So when the rate cutting started, longer-term yields went the opposite way: They jumped amid resurfacing inflation fears, and mortgage rates spiked.

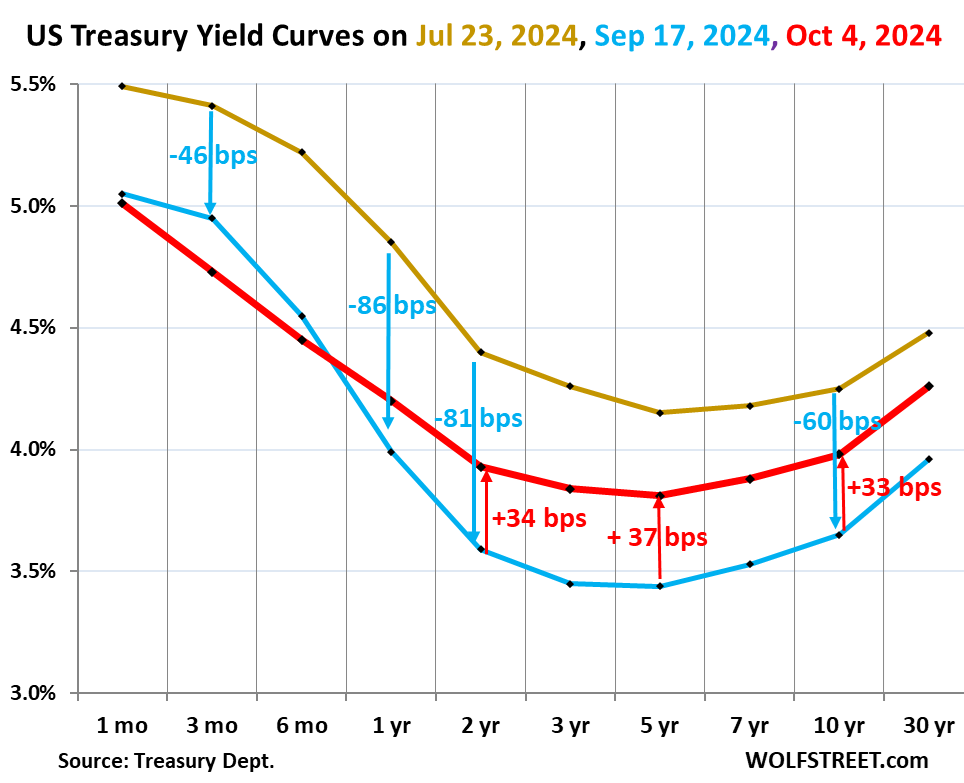

The chart shows the “yield curve,” with Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 23, before the labor market data went into a tailspin.

- Blue: September 17, the day before the mega-rate cut.

- Red: October 4, after the jobs report.

As shorter-term yields stayed roughly put over the past days while longer-term yields jumped, the yield curve un-inverted further – it became somewhat flatter. Eventually, the yield curve will enter its normal state where shorter-term yields are lower than longer-term yields across the yield curve. But it still has aways to go.

Between July 23 (gold) and September 17 (blue), yields plunged across the yield curve in anticipation of lots of rate cuts from the Fed – thereby pricing in a bunch of future rate cuts (blue figures and down arrows in the chart above):

- 3-month: -46 basis points

- 1-year: -86 basis points

- 2-year: -81 basis points

- 3-year: -81 basis points

- 5-year: -71 basis points

- 10-year: -60 basis points

- 30-year: -52 basis points

From September 17 (blue) to October 4 (red), from the day before the rate cut to Friday, October 4 (red figures and up-arrows in the chart above):

- 3-month: -22 basis points

- 1-year: +21 basis points

- 2-year: +34 basis points

- 3-year: +39 basis point

- 5-year: +37 basis points

- 10-year: +33 basis points

- 30-year: +11 basis points

Yields jumped the most in the middle on crushed rate-cut expectations.

The 1-year yield, which had been as low as 3.88% on September 24, is back at 4.20%, after Friday’s 18 basis-point jump.

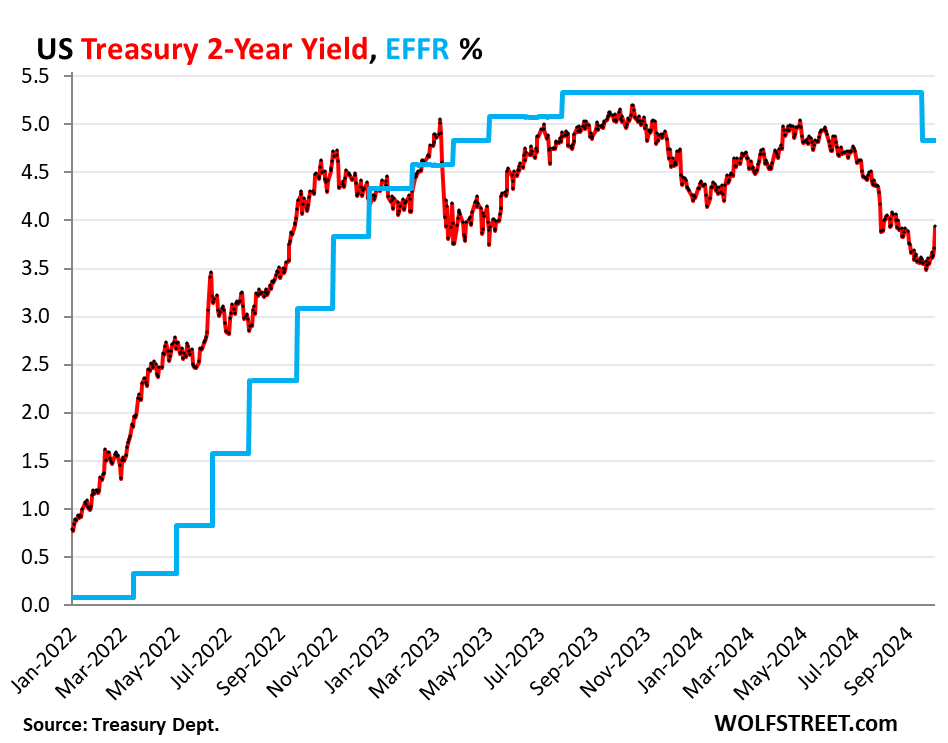

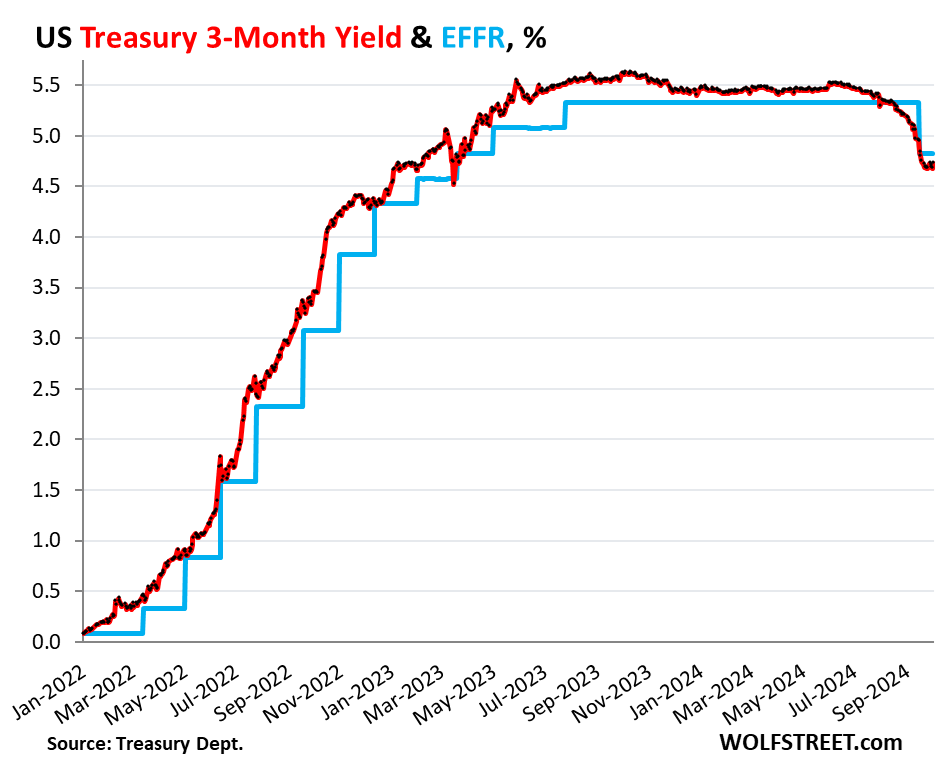

The effective federal funds rate (EFFR) which the Fed targets with its headline policy target range, dropped 50 basis points after the Fed announced its 50-basis-point rate cut, from 5.33% on Wednesday September 18, to 4.83% the next day, and it has remained there since (blue in the charts).

The biggest jump on Friday occurred at the 2-year yield, which spiked by 23 basis points, to 3.93%. Over the past two days combined, it spiked by 30 basis points. This shows that markets have dialed back their aggressive rate-cut expectations with which they had gone into the September 18 FOMC meeting. Quite a U-turn (EFFR = effective federal funds rate which the Fed targets with its policy target range):

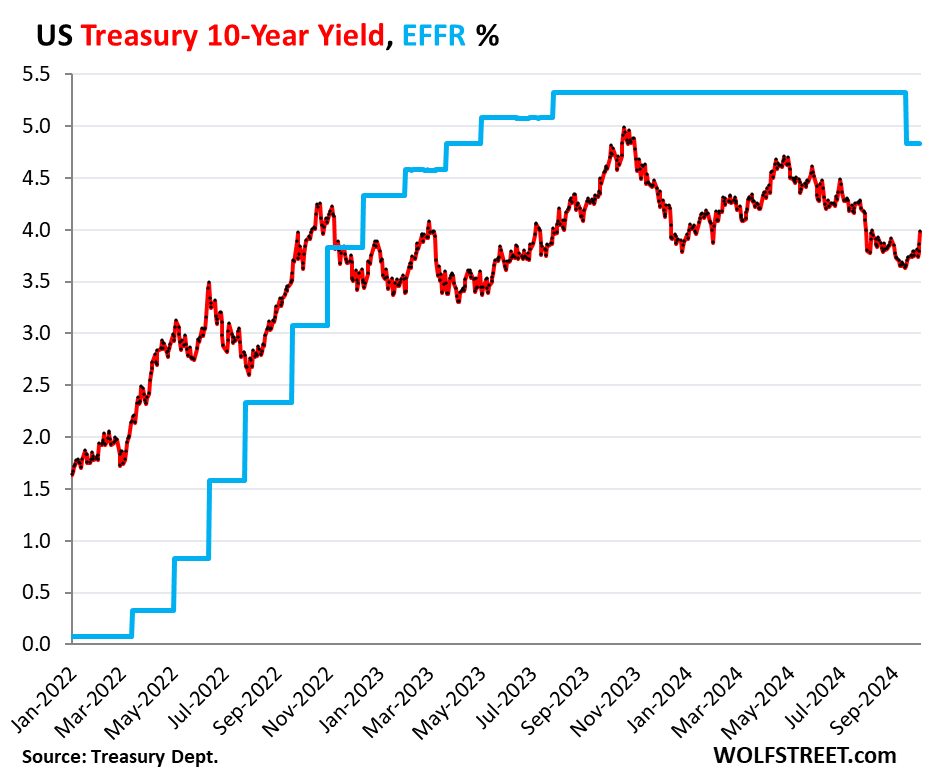

The 10-year yield jumped by 13 basis points on Friday and has risen by 33 basis points since the rate cut, to 3.98%. It’s back where it had last been on August 8.

The 10-year yield isn’t as much a reflection of rate cuts and rate-cut expectations, which impact short-term yields, but more a reflection of inflation expectations over the next 10 years. And there are all kinds of dynamics under way now that indicate that inflation might not go back to sleep. We got the latest indication in the jobs report: steep increases of average hourly earnings in August and September.

In addition, the 10-year yield is a reflection of expected supply, and given the massively ballooning US debt, supply will be huge, everyone knows that.

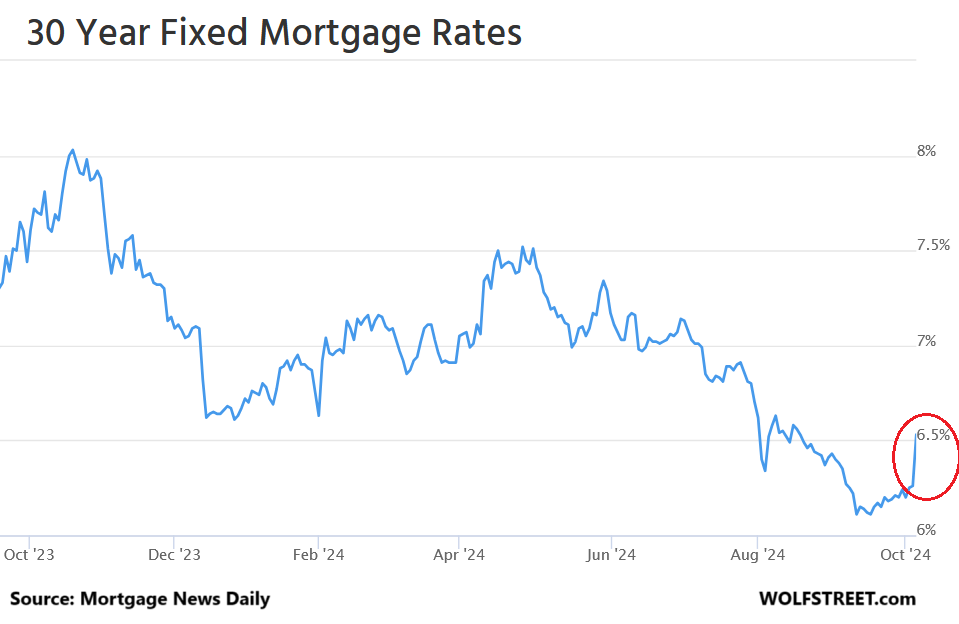

The average 30-year fixed mortgage rate exploded on Friday by 27 basis points to 6.53%, according to Mortgage News Daily. It was quite a mess (chart via Mortgage News Daily).

Mortgage rates roughly parallel the 10-year yield but at a higher level. The spread between the average 30-year mortgage rate and the 10-year yield has been around 2.5 percentage points all year, which is higher than average over the past four decades, in a range that went from near 0 percentage points to over 4 percentage points.

With the 10-year yield 3.98% on Friday, and the average 30-year fixed mortgage rate at 6.53%, the spread between the two measures was 2.55 percentage points.

The spread could remain in this wider range because the Fed no longer supports the mortgage market, as it had done during QE. As part of QT, it is letting its holdings of MBS run off at the pace of the passthrough principal payments, and it’s letting its holdings of Treasury securities run off at a pace of $25 billion a month. In September, the Fed’s total assets fell by $66 billion, to $7.05 trillion.

The Fed said it would let the MBS run entirely off its balance sheet even after QT ends, which would take years, and market participants will have to be enticed to take the Fed’s place, and this could mean that the spread will average wider than during the era of QE.

Despite the drama on the long end, not much happened at the short end.

Short-term yields are pricing in the expected rate cuts during their term. A security with 3-months left to run will trade on expectations of rates largely over the next two months. The closer the security gets toward its maturity date, the less policy rates matter because on maturity date, the holder will get paid face value plus interest. And that’s the value of the security on that day, no matter what policy rates are.

The 3-month yield rose by 5 basis points on Friday, to 4.73%. But it has vacillated in this range for about two weeks. It has fully priced in one 25-basis-point cut, plus portions of a second 25-basis point cut. The yield is down 22 basis points from September 17.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More: Mortgage Rates Explode, 2-Year & 10-Year Treasury Yields Spike, Monster Rate-Cut Hopes