More evidence that underlying inflation dynamics are thriving.

By Wolf Richter for WOLF STREET.

How corporate profits spiked during the inflation-shock of 2021 and 2022 was amazing to watch: The pricing power companies suddenly had to hike prices and pump up profits because their customers were suddenly paying whatever, thereby propagating inflation across the economy. Then pricing power started fading, a mini lull ensued, and inflation backed off a lot. But now corporate profits have taken off again, and this renewed pricing power could be more bad news on the inflation front.

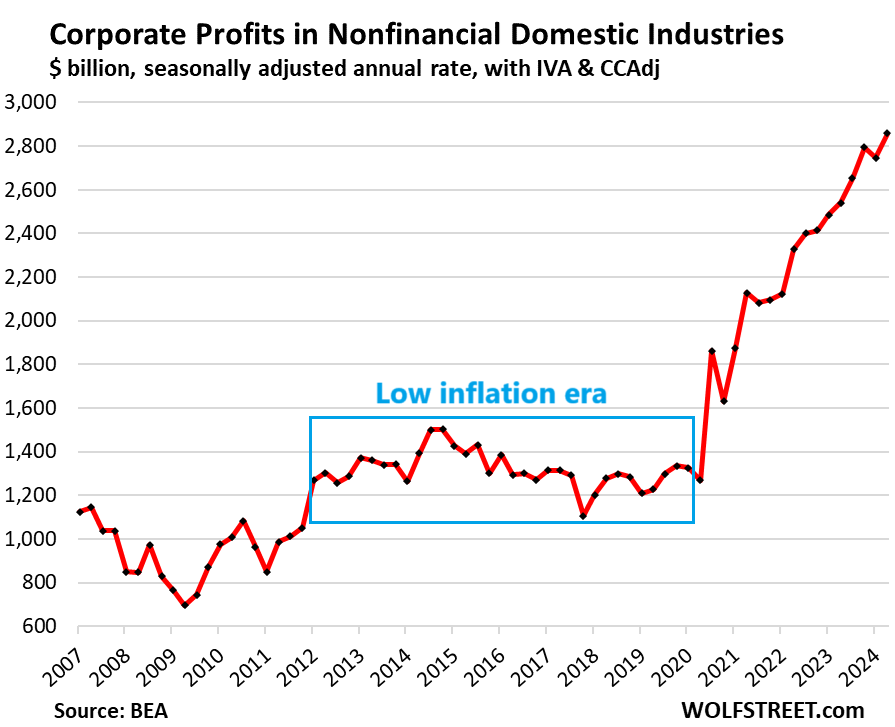

Corporate pre-tax profits in nonfinancial domestic industries – all businesses except financial firms such as banks, insurers, etc. – jumped by 4.1% in Q2 from Q1, and by 12.5% year-over-year, to a seasonally adjusted annual rate of $2.86 trillion, having spiked by 125% since Q2 2020, according to the by-industry data released today by the Bureau of Economic Analysis.

These are pre-tax profits “from current production” by all nonfinancial businesses that have to file corporate tax returns, including LLCs and S corporations, plus some organizations that do not file corporate tax returns. The BEA obtains this information from IRS income tax data and from financial statements filed with the SEC.

Note in the chart above how the current surge contrasts with how well-behaved the line was before 2020. That era of low inflation is gone.

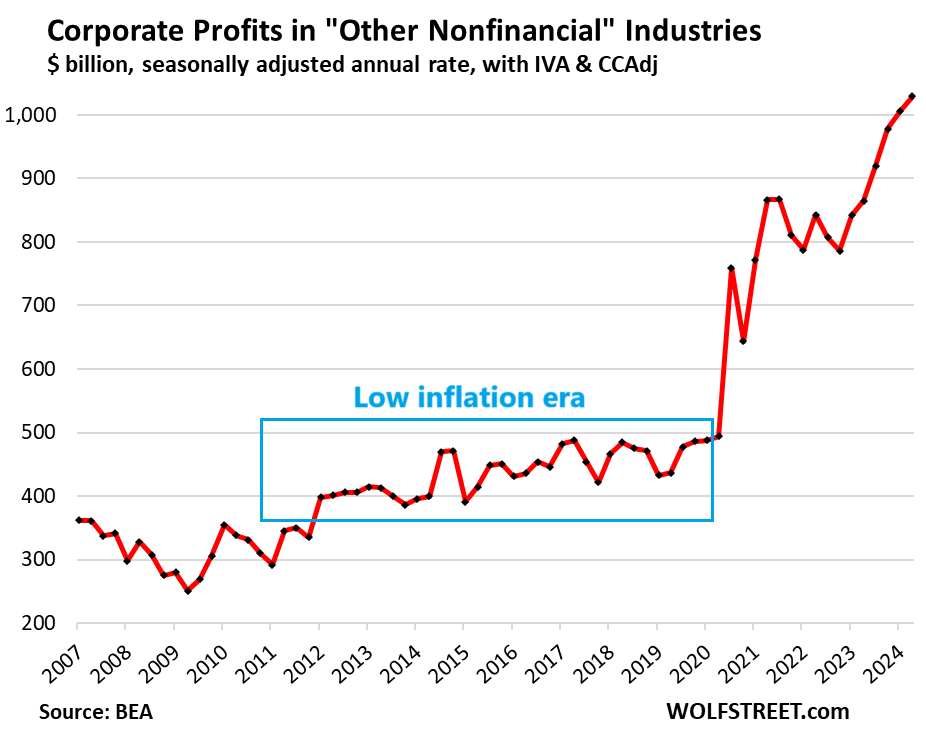

“Other nonfinancial” industries: Profits jumped by 2.2% in Q2 from Q1 and by 19.0% year-over-year, to a seasonally adjusted annual rate of $1.03 trillion. Since Q1 2020, profits have spiked by 109% as businesses raised prices far faster than their costs had risen, and their customers – other businesses and consumers – just paid whatever. Note the surge after the lull.

This is the biggest category in the BEA data with huge industries, including construction; professional, scientific, and technical services (where some of the tech and social media companies are); healthcare and social assistance; real estate and rental and leasing; accommodation and food services; mining and oil-and-gas drilling; administrative and waste management services; educational services; arts, entertainment, and recreation; agriculture, forestry, fishing, and hunting.

This is what big inflation is all about: Businesses are raising prices far faster than their costs go up, because suddenly they can, because suddenly their customers (consumers and other businesses), befuddled by the new inflationary mindset, are willing to pay whatever. Workers in turn clamor for higher wages to meet the higher prices. Companies, having discovered their pricing power and using it, are willing to pay higher wages to keep and attract talent.

These corporate profits and other indicators tell us that pricing power and paying whatever – and thereby inflation – are far from vanquished.

It’s the Fed’s job to knock some sense back into these economic players – companies and consumers – by making the cost of capital painfully high, and it did that by hiking rates far higher than most economists had expected and keeping them there far longer than they’d expected.

But long-term interest rates started falling 10 months ago, in anticipation that the Fed would back off, and now it has started to back off. So we’ll see how far the Fed can go with it before inflation re-heats up to worrisome levels for all to see.

How are these profits figured? These pre-tax profits “from current production” are based on IRS tax return data and SEC filings but have been adjusted in three ways:

- IVA (“inventory valuation adjustment”) removes profits derived from inventory cost changes, which are more like capital gains rather than profits “from current production.”

- CCAdj (“capital consumption adjustment”) converts the tax-return measures of depreciation to measures of consumption of fixed capital, based on current cost with consistent service lives and with empirically based depreciation schedules.

- Capital gains & dividends are excluded to show profits “from current production,” rather than financial gains.

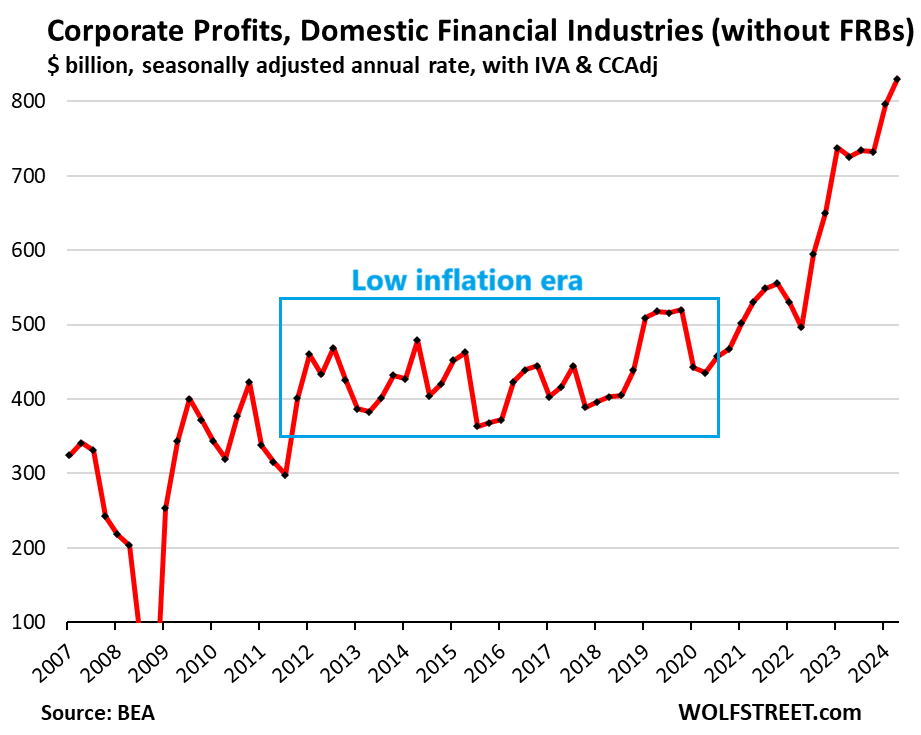

Financial Industries (domestic): Profits spiked by 4.2% in Q2 from Q1 and by 14.4% year-over-year to a seasonally adjusted annual rate of $830 billion.

The financial industry includes banks and bank holding companies, plus firms engaged in other credit intermediation and related activities; firms engaged in securities, commodity contracts, and other financial investments and related activities; insurance carriers; funds, trusts, and other financial vehicles. But this metric does not include the 12 regional Federal Reserve Banks (FRBs).

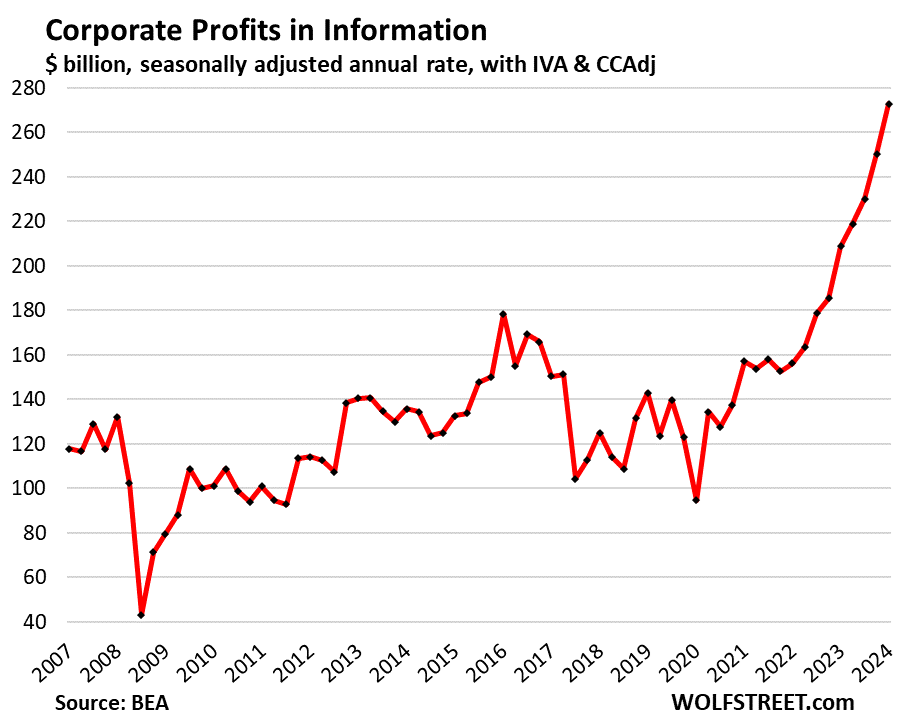

Information: Profits spiked by 8.9% in Q2 from Q1 and by 30.6% year-over-year, to a seasonally adjusted annual rate of $273 billion.

The sector includes many tech and social media companies. Businesses are engaged in web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

Trimming costs by slashing their payrolls – as tech and social media companies have done in San Francisco and Silicon Valley – must have helped boost profits, in addition to raising prices. Profits have spiked in just two years by 80%:

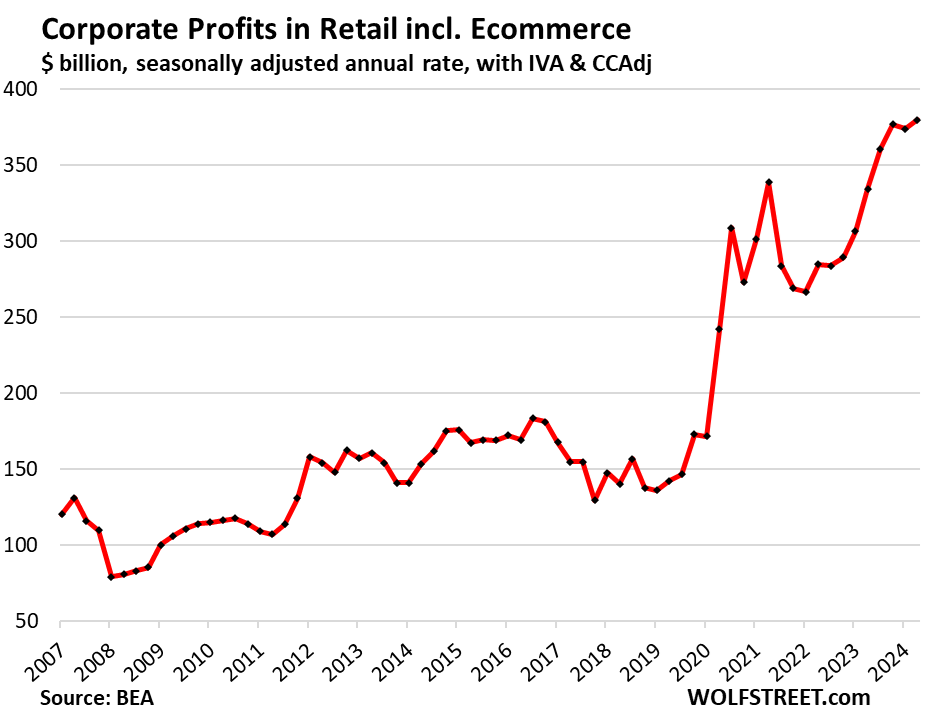

Retail trade, including Ecommerce: Profits rose by 1.6% in Q2 from Q1 and by 13.5% year-over-year, to a seasonally adjusted annual rate of $380 billion, a new record, up 122% since Q1 2020:

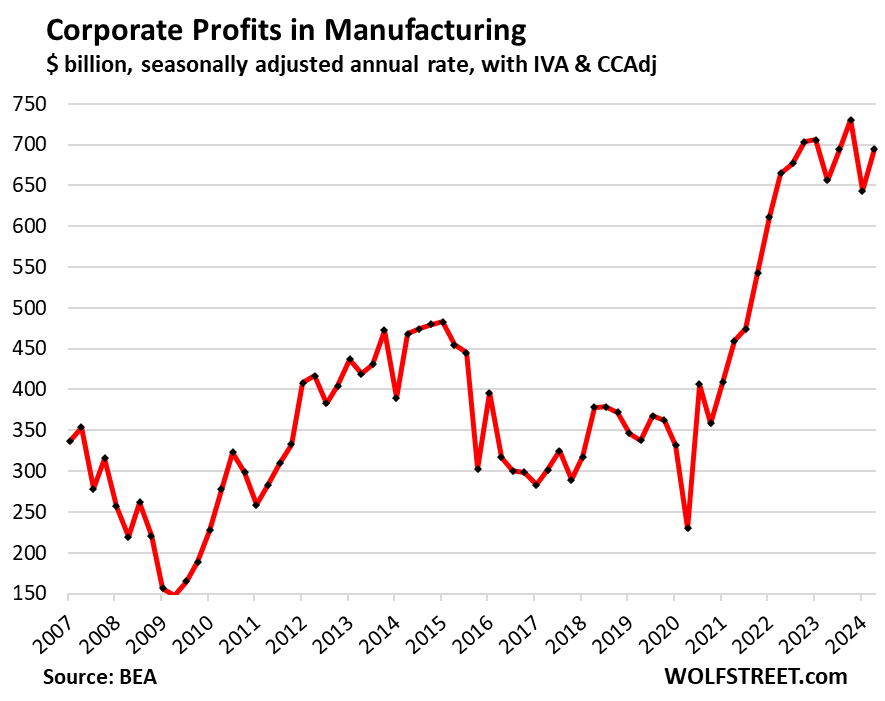

Manufacturing industries: Profits rose by 5.9% in Q2 from Q1 and by 8% year-over-year, to a seasonally adjusted annual rate of $695 billion.

This includes manufacturing of durable goods (computers, electronics, electrical equipment, appliances, motor vehicles, trailers, machinery, fabricated metals, components, etc.) and nondurable goods (food, beverages, supplies, petroleum products (including gasoline and diesel), coal products; chemical products, etc.).

The big increase in Q2 didn’t quite undo the sharp drop in Q1 off the record in Q4 2023. What’s surprising is that profits in manufacturing are still so high:

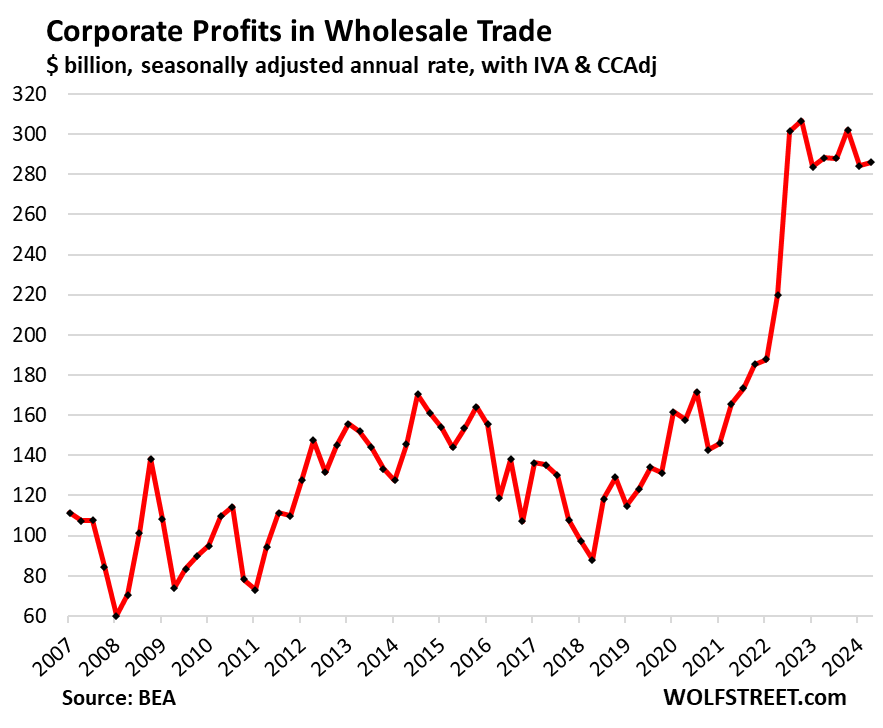

Wholesale trade: Profits dipped by 0.8% in Q2 from Q1, to a seasonally adjusted annual rate of $286 billion. Year-over-year, profits inched up 0.6%. In this industry, profits have remained very high after the huge spike in the first half of 2022, but they have not grown further since then:

Transportation & warehousing: Profits dipped in Q2 from Q1, to $129 billion, and were unchanged year-over-year, at very high and near-record levels after the huge spike.

![]()

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

Read More: Corporate Pricing Power and Therefore Inflation Not Vanquished, Says Renewed Spike in